Canada Goose Holdings (GOOS) is breaking out higher on stronger fundamental operations. The company continues to experience strong demand for its products, alongside management improving on its operational efficiency, driving bottom-line performance. Its share price is breaking out higher after months of consolidation. I am buying stock in this name as its fundamentals justify further price appreciation.

Fundamental Narrative

GOOS looks attractively positioned at current levels as it is experiencing strong demand for its products, driving top-line growth, alongside management's improved efficiency, similarly driving its bottom-line higher.

The company designs, manufactures, and sells premium outdoor apparel for men, women, youth, children, and babies in Canada, the United States, and internationally. They operate in two segments, Wholesale and Direct to Consumer. It offers parkas, jackets, shells, vests, knitwear, and accessories for fall, winter, and spring seasons. The company sells its products through online retailers and distributors; and its e-commerce sites and retail stores.

Over the most recent quarter, revenue increased by 27.2% to 265.8 million, driven by growth across all channels, geographies and categories, signaling the company's impressive growth trajectory. Direct-to-consumer or D2C revenue came in at 131.6 million including strong performance from its four new stores which opened during the quarter as well as continued strength from its existing e-commerce sites and stores, according to its earnings call. As a percentage of total revenue, D2C was 49.5% compared to 34.4% last year, signaling that its operations are quickly migrating towards such channels.

Demand for its products remains high as customers across all regions and climates have responded well to the innovation and quality of the product in its fall/winter line, according to management.

GOOS saw strong sales in both core and new styles across both its men's and women's businesses in recent quarters. For example, its classic expedition parka is a style that they have offered for decades yet sales continue to increase year over year, according to its earnings call. At the same time, the company continues to see growing demand for its lightweight down product, another testament to its increasing relevance in more temperate climates, as well as its ability to successfully expand its product ramp.

According to management, more people today see outerwear as a prominent part of their wardrobe, not just buying one fall or winter coat anymore. Customers are looking for a variety different colors, silhouettes and fits, leading GOOS to introduce over 30 new styles in recent years. Another example of this is the company's Fusion Fit, introduced in 2014 to address the diversity of body frames around the world. The brand has been growing steadily since its launch with significant unit growth in recent quarters, according to its earnings call.

As far as geographic growth, expanding internationally is an important part of its growth strategy with management executing well so far. They grew revenue significantly in all of its geographic segments over the last quarter, on top of robust growth in its home market. Over the past year, GOOS has had customers from 87 different countries. Meanwhile, when you look at its penetration level in Canada, which continues to grow at a very healthy rate, it is clear that they continue to have a compelling opportunity to drive growth while expanding access to its product around the world, according to its earnings call.

More specifically, there also looks to be opportunity in China with continued demand potential in that market. In its stores and online, the company has experienced exceptional demand from Chinese tourists, students and/or residents, which has helped inform management's understanding of the end market opportunity there and how to best meet those needs. Its strategy looks to be set, with management already executing on its go-to-market strategy in China, working diligently to reach wholesale e-commerce and store pieces in place.

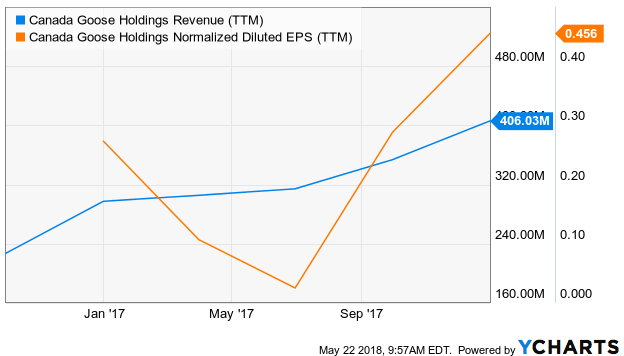

Below is a chart of both GOOS's revenue and earnings per share. Over the last two years, both revenue and EPS have risen significantly, signaling strong demand for the company's products, as well as management's improving efficiency. Revenue has roughly doubled, while its EPS fell to near zero, now reaching nearly $0.5 in EPS. Improving fundamental results should continue to fuel improving investor sentiment in coming quarters.

Price Action

GOOS's share price has been in a steady trend higher alongside strong demand for its products. Although its trend has been stable, recent broader market volatility led to a consolidation in the company's share price, creating a buying opportunity. A combination of stabilizing equity markets and strong earnings results led GOOS to breakout above its $38 level, which had acted as a resistance area in recent months. Its price momentum should continue in coming quarters as its operational results are fueling the current trend higher.

Conclusion

GOOS is breaking out higher on stronger fundamental operations. The company continues to experience strong demand for its products, with management improving on its operational efficiency, driving bottom-line performance. Its share price is breaking out higher after months of consolidation. I am buying stock in this name as its fundamentals justify further price appreciation.

Markets move quickly. To take advantage of the highs and lows - especially in today's volatile environment - you need a strategy that's nimble and flexible. My approach is both, and it enables me to move in and out of assets and sectors while continually generating double-digit annualized returns. Sign up for Absolute Returns today to see how I manage my portfolio in the continuously changing market environment. Many believe absolute returns and beating the market are mere fiction, but I assure you they're not. See for yourself how you can benefit from my approach, and how your portfolio can profit, regardless of market conditions.

Disclosure: I am/we are long GOOS.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

DigiCube (CURRENCY:CUBE) traded down 0.3% against the US dollar during the twenty-four hour period ending at 12:00 PM ET on June 23rd. During the last week, DigiCube has traded down 51.9% against the US dollar. DigiCube has a total market capitalization of $149,052.00 and $2.00 worth of DigiCube was traded on exchanges in the last 24 hours. One DigiCube coin can now be purchased for $0.0001 or 0.00000001 BTC on cryptocurrency exchanges.

DigiCube (CURRENCY:CUBE) traded down 0.3% against the US dollar during the twenty-four hour period ending at 12:00 PM ET on June 23rd. During the last week, DigiCube has traded down 51.9% against the US dollar. DigiCube has a total market capitalization of $149,052.00 and $2.00 worth of DigiCube was traded on exchanges in the last 24 hours. One DigiCube coin can now be purchased for $0.0001 or 0.00000001 BTC on cryptocurrency exchanges.