Investors in Devon Energy (NYSE: DVN ) are probably pretty pleased with the pipeline partnership deal it just inked with Crosstex Energy, but investors need to know what Devon must do to remain successful past this one-off agreement. For the natural gas and oil producer to stay on top of the U.S. shale drilling game, it will need to shift its focus away from the Barnett shale to the Permian Basin.�

Both Devon and Pioneer Natural Resources (NYSE: PXD ) have been pulling out of the Barnett recently for good reason -- the economics for wells just aren't there based on today's gas prices. So Devon and Pioneer have set their sights on the Permian instead. Devon already has a major presence in the Permian, so ramping up activity there should be easier than at many of its other holdings across the country. In the video below, Fool contributor Tyler Crowe discusses the other reasons why Devon will need the Permian going forward.�

Who Will Join Devon in Dominating the American Energy Boom?

Devon is carving out a position as a top American energy company, but they aren't alone. The transformation of the American energy space is creating investment opportunities everywhere, but picking the right ones will mean the difference between a flash in the pan and a long term jewel. For this reason, we have put together comprehensive look at three energy companies set to soar during this transformation in the energy industry. Find out which two companies have joined Devon on our list of companies that are spreading their wings by checking out our special report, "3 Stocks for the American Energy Bonanza." Simply�click here�and we'll give you free access to this valuable investing resource.�

Top Oil Stocks To Own For 2014: Occidental Petroleum Corporation(OXY)

Occidental Petroleum Corporation, together with its subsidiaries, operates as an oil and gas exploration and production company primarily in the United States. The company operates in three segments: Oil and Gas; Chemical; and Midstream, Marketing, and Other. The Oil and Gas segment explores for, develops, produces, and markets crude oil, natural gas liquids, and condensate and natural gas. Its domestic oil and gas operations are located in Texas, New Mexico, California, Kansas, Oklahoma, Utah, Colorado, North Dakota, and West Virginia; and international oil and gas operations are located in Bahrain, Bolivia, Colombia, Iraq, Libya, Oman, Qatar, the United Arab Emirates, and Yemen. As of December 31, 2010, this segment had proved reserves of approximately 3,363 million barrels of oil equivalent. The Chemical segment manufactures and markets basic chemicals, including chlorine, caustic soda, chlorinated organics, potassium chemicals, and ethylene dichloride products; vinyls, such as vinyl chloride monomer and polyvinyl chloride; and other chemicals comprising chlorinated isocyanurates, resorcinol, sodium silicates, and calcium chloride products. The Midstream, Marketing, and Other segment gathers, treats, processes, transports, stores, purchases, and markets crude oil that includes natural gas liquids and condensate, as well as natural gas and carbon dioxide. This segment also involves in the power generation; and trades around its assets comprising pipelines and storage capacity, as well as oil and gas, other commodities, and commodity-related securities. Occidental Petroleum Corporation was founded in 1920 and is based in Los Angeles, California.

Advisors' Opinion:- [By Federico Zaldua]

Occidental Petroleum (OXY), just bought by George Soros for his family-owned hedge fund, is more highly leveraged into oil than most of its large exploration and production (E&P) peers. That said, the company presented slightly disappointing quarterly earnings. Earnings were down 4% from a year ago and 7% sequentially despite the good results at the oil and gas division. Nevertheless, the future performance of the stock will mainly depend on what the board decides about corporate restructuring.

- [By Sean Williams]

In the Permian Basin, Occidental Petroleum (NYSE: OXY ) has been a big rail transport beneficiary, since it produced as much oil in 2011 as the No. 2, No. 3, and No. 4 producers combined! Being able to pilfer a few extra dollars per barrel can mean hundreds of millions of dollars extra for companies like Occidental with huge oil exposure.

Top Oil Stocks To Own For 2014: Chesapeake Energy Corporation(CHK)

Chesapeake Energy Corporation engages in the acquisition, development, exploration, and production of natural gas and oil properties in the United States. It also provides marketing and other midstream services. The company?s properties are located in Alabama, Arkansas, Colorado, Kansas, Kentucky, Louisiana, Maryland, Michigan, Mississippi, Montana, Nebraska, New Mexico, New York, North Dakota, Ohio, Oklahoma, Pennsylvania, Tennessee, Texas, Utah, Virginia, West Virginia, and Wyoming. As of December 31, 2010, it had interests in approximately 45,800 gross productive wells. The company?s proved reserves include 17.096 trillion cubic feet of natural gas equivalent. Chesapeake Energy Corporation was founded in 1989 and is based in Oklahoma City, Oklahoma.

Advisors' Opinion:- [By Arjun Sreekumar]

Last week, Chesapeake Energy (NYSE: CHK ) reported a first-quarter profit that beat Wall Street expectations, aided by strong oil production growth and higher natural gas prices during the quarter.

- [By Matt DiLallo]

Because of the lackluster returns so far, major oil and gas producers like Chesapeake Energy (NYSE: CHK ) and Devon Energy (NYSE: DVN ) have announced plans to reduce operations in the play. Devon, which is completely exiting the play, really had a rough year, as most of the wells it drilled were not economical. One of the issues is the oil accumulations located in the shale were in areas that lacked the pressure necessary to force the oil out of the shale. Chesapeake, on the other hand, is selling what is no longer core acreage in order to shore up its balance sheet.

- [By WALLSTCHEATSHEET.COM]

Chesapeake is definitely on the correct path. However, it might be too little too late. If the global economy continues to weaken, then Chesapeake will have to fight hard just to break even. In the current economic environment, the majors like Exxon Mobil (NYSE:XOM) and Chevron Corporation (NYSE:CVX) are safer alternatives.

- [By Dan Caplinger]

Perhaps most importantly, Ultra hasn't made the same mistakes as some of its formerly gas-focused competitors in buying high and selling low. Chesapeake Energy (NYSE: CHK ) and SandRidge Energy (NYSE: SD ) largely gave up on gas, seeking to broaden their asset bases further into more lucrative oil and natural gas liquids. Yet as Chesapeake and SandRidge have sold off assets at the least desirable time, Ultra has stayed committed to gas and therefore stands to benefit more from its recent gains.

Top 10 Value Stocks To Buy Right Now: Falcon Oil & Gas Ltd (FO)

Falcon Oil & Gas Ltd. (Falcon) is an energy company engaged in the business of acquiring, exploring and developing petroleum and natural gas properties. The Company focuses on the acquisition, exploration and development of conventional and unconventional petroleum and natural gas projects in Central Europe (specifically Hungary), Australia and South Africa. Falcon holds 100% interest in 245,775 acres in a production license in the Mako Trough, southern Pannonian Basin in Hungary. Effective July 18, 2013, Falcon Oil & Gas Ltd raised its interest to 96.9% from 72.68%, by acquiring a further 24.22% interest in Falcon Oil & Gas Australia Ltd, from Sweetpea Petroleum Corp Pty Ltd, a unit of PetroHunter Energy Corp. Effective September 19, 2013, Falcon Oil & Gas Ltd acquired the remaining 3.1% stake, which it did not already own, in Falcon Oil & Gas Australia Ltd, a oil and gas exploration and production company.Top Oil Stocks To Own For 2014: Access Midstream Partners LP (ACMP)

Access Midstream Partners, L.P., formerly Chesapeake Midstream Partners, L.L.C. (Partnership), incorporated on January 21, 2010, owns, operates, develops and acquires natural gas, natural gas liquids (NGLs) and oil gathering systems and other midstream energy assets. The Company is focused on natural gas and NGL gathering. The Company provides its midstream services to Chesapeake Energy Corporation (Chesapeake), Total E&P USA, Inc. (Total), Mitsui & Co. (Mitsui), Anadarko Petroleum Corporation (Anadarko), Statoil ASA (Statoil) and other producers under long-term, fixed-fee contracts. On December 20, 2012, the Company acquired from Chesapeake Midstream Development, L.P. (CMD), a wholly owned subsidiary of Chesapeake, and certain of CMD's affiliates, 100% of interests in Chesapeake Midstream Operating, L.L.C. (CMO). As a result of the CMO Acquisition, the Partnership owns certain midstream assets in the Eagle Ford, Utica and Niobrara regions. The CMO Acquisition also extended the Company's assets and operations in the Haynesville, Marcellus and Mid-Continent regions.

The Company operates assets in Barnett Shale region in north-central Texas; Eagle Ford Shale region in South Texas; Haynesville Shale region in northwest Louisiana; Marcellus Shale region in Pennsylvania and West Virginia; Niobrara Shale region in eastern Wyoming; Utica Shale region in eastern Ohio, and Mid-Continent region, which includes the Anadarko, Arkoma, Delaware and Permian Basins. The Company's gathering systems collect natural gas and NGLs from unconventional plays. The Company generates its revenues through long-term, fixed-fee gas gathering, treating and compression contracts and through processing contracts.

Barnett Shale Region

The Company's gathering systems in its Barnett Shale region are located in Tarrant, Johnson and Dallas counties in Texas in the Core and Tier 1 areas of the Barnett Shale and consist of 25 interconnected gathering systems and 850 miles of pipeline. During the year! ended December 31, 2012, average throughput on the Company's Barnett Shale gathering system was 1.195 billion cubic feet per day. The Company connects its gathering systems to receipt points that are either at the individual wellhead or at central receipts points into which production from multiple wells are gathered. The Company's Barnett Shale gathering system is connected to the three downstream transportation pipelines: Atmos Pipeline Texas, Energy Transfer Pipeline Texas and Enterprise Texas Pipeline. Natural gas delivered into Atmos Pipeline Texas pipeline system serves the greater Dallas/Fort Worth metropolitan area and south, east and west Texas markets at the Katy, Carthage and Waha hubs. Natural gas delivered into Energy Transfer Pipeline Texas pipeline system serves the greater Dallas/Fort Worth metropolitan area and southeastern and northeastern the United States markets supplied by the Midcontinent Express Pipeline, Centerpoint CP Expansion Pipeline and Gulf South 42-inch Expansion Pipeline. Natural gas delivered into Enterprise Texas Pipeline pipeline system serves the greater Dallas/Fort Worth metropolitan area and southeastern and northeastern the United States markets supplied by the Gulf Crossing Pipeline.

Eagle Ford Shale Region

The Company's gathering systems in its Eagle Ford Shale region are located in Dimmit, La Salle, Frio, Zavala, McMullen and Webb counties in Texas and consist of 10 gathering systems and 618 miles of pipeline. During 2012, gross throughput for these assets was 0.169 billion cubic feet per day. The Company connects its gathering systems to central receipt points into which production from multiple wells is gathered. The Company's Eagle Ford gathering systems are connected to six downstream transportation pipelines, which include Enterprise, Camino Real, West Texas Gas, Regency Gas Service, Eagle Ford Gathering and Enerfin. The Company processes gas at Yoakum or other Enterprise plants and transports residue to Wharton residue header w! ith conne! ctions to numerous interstate pipelines.

Haynesville Shale Region

The Company's Springridge gas gathering system in the Haynesville Shale region is located in Caddo and DeSoto Parishes, Louisiana, in one of the core areas of the Haynesville Shale and consists of 263 miles of pipeline. During 2012, average throughput on the Company's Springridge gathering system was 0.359 billion cubic feet per day. The Company connects its gathering system to receipt points that are at central receipt points into which production from multiple wells is gathered. The Company's Springridge gathering system is connected to three downstream transportation pipelines: Centerpoint Energy Gas Transmission, ETC Tiger Pipeline and Texas Gas Transmission Pipeline. The Company's Mansfield gas gathering system in the Haynesville Shale region is located in DeSoto and Sabine Parishes, Louisiana, in one of the areas of the Haynesville Shale and, as of December 31, 2012, consist of 304 miles of pipeline. During 2012, average throughput on the Company's Mansfield gathering system was 0.720 billion cubic feet per day. The Company connects its gathering system to receipt points that are at central receipt points into which production from multiple wells is gathered and treated. The Company's Mansfield gathering system is connected to two downstream transportation pipelines: Enterprise Accadian Pipeline and Gulf South Pipeline. Natural gas delivered into Enterprise Accadian pipeline can move to on-system markets in the Midwest and to off-system markets in the Northeast through interconnections with third-party pipelines. Natural gas delivered into Gulf South pipeline can move to on-system markets in the Midwest and to off-system markets in the Northeast through interconnections with third-party pipelines.

Marcellus Shale Region

Through Appalachia Midstream, the Company operates 100% of and own an approximate average 47% interests in 10 gas gathering systems that consist of approximately 5! 49 miles ! of gathering pipeline in the Marcellus Shale region. The Company's volumes in the region are gathered from northern Pennsylvania, southwestern Pennsylvania and the northwestern panhandle of West Virginia, in core areas of the Marcellus Shale. The Company operates these smaller systems in northeast and central West Virginia, southeast Pennsylvania, northwest Maryland, north central Virginia, and south central New York. During 2012, gross throughput for Appalachia Midstream assets was just over 1.8 billion cubic feet per day. The Company's Marcellus gathering systems' delivery points include Caiman Energy, Central New York Oil & Gas, Columbia Gas Transmission, MarkWest, NiSource Midstream, PVR and Tennessee Gas Pipeline. Natural gas is delivered into a 16-inch pipeline and delivered to the Caiman Energy Fort Beeler processing plant where the liquids are extracted from the gas stream. The natural gas is then delivered into the TETCo interstate pipeline for ultimate delivery to the Northeast region of the United States. Natural gas delivered into Central New York Oil & Gas 30-inch diameter pipeline can be delivered to Stagecoach Storage, Millennium Pipeline, or Tennessee Gas Pipeline's Line 300. In Columbia Gas Transmission lean natural gas is delivered into two 36-inch interstate pipelines for delivery to the Mid-Atlantic and Northeast regions of the United States. Natural gas is delivered into a MarkWest pipeline for delivery to the MarkWest Houston processing plant where the liquids are extracted from the gas stream. In NiSource Midstream natural gas is delivered into a 20-inch diameter pipeline and delivered to the MarkWest Majorsville processing plant where the liquids are extracted from the rich gas stream. In PVR natural gas is delivered into the 24-inch diameter Wyoming pipeline and the Hirkey Compressor Station. In Tennessee Gas Pipeline natural gas is delivered into this looped 30-inch diameter pipeline (TGP Line 300) at three different locations can be received in the Northeast at points along th! e 300 Lin! e path, interconnections with other pipelines in northern New Jersey, as well as an existing delivery point in White Plains, New York.

Niobrara Shale Region

The Company's gathering systems in the Niobrara Shale region are located in Converse County, Wyoming and consist of two interconnected gathering systems and 79 miles of pipeline. During 2012, average throughput in the Company's Niobrara Shale region was 0.013 billion cubic feet per day. The Company connects its gathering systems to receipt points,which are either at the individual wellhead or at central receipts points into which production from multiple wells are gathered. The Company's Niobrara gathering systems are connected to two downstream transportation pipelines: Tallgrass/Douglas Pipeline and North Finn/DCP Inlet Pipeline. Natural gas delivered into Tallgrass/Douglas pipeline is sent to the Tallgrass processing facility; after processing, natural gas is delivered to Cheyenne Hub, Rockies Express Pipeline, or Trailblazer Pipeline through Tallgrass Interstate Gas Transmission.

Utica Shale Region

The Company's gathering systems in the Utica Shale region are located in northeast Ohio and consist of 67 miles of pipeline. The Company's Utica gathering systems are connected to two downstream transportation pipelines: Dominion East Ohio (Blue Racer) and Dominion Transmission, Inc.

Mid-Continent Region

The Company's Mid-Continent gathering systems extend across portions of Oklahoma, Texas, Arkansas and Kansas. Included in the Company's Mid-Continent region are three treating facilities located in Beckham and Grady Counties, Oklahoma, and Reeves County, Texas, which are designed to remove contaminants from the natural gas stream.

Anadarko Basin and Northwest Oklahoma

The Company's assets within the Anadarko Basin and Northwest Oklahoma are located in northwestern Oklahoma and the northeastern portion of the Texas Panhandle and consist of appro! ximately ! 1,578 miles of pipeline. During 2012, the Company's Anadarko Basin and Northwest Oklahoma region gathering systems had an average throughput of 0.457 billion cubic feet per day. Within the Anadarko Basin and Northwest Oklahoma, the Company is focused on servicing Chesapeake's production from the Colony Granite Wash, Texas Panhandle Granite Wash and Mississippi Lime plays. Natural gas production from these areas of the Anadarko Basin and Northwest Oklahoma contains NGLs. In addition, the Company operates an amine treater with sulfur removal capabilities at its Mayfield facility in Beckham County, Oklahoma. The Company's Mayfield gathering and treating system gathers Deep Springer natural gas production and treats the natural gas to remove carbon dioxide and hydrogen sulfide to meet the specifications of downstream transportation pipelines.

The Company's Anadarko Basin and Northwest Oklahoma systems are connected to a transportation pipelines transporting natural gas out of the region, including pipelines owned by Enbridge and Atlas Pipelines, as well as local market pipelines such as those owned by Enogex. These pipelines provide access to Midwest and northeastern the United States markets, as well as intrastate markets.

Permian Basin

The Company's Permian Basin assets are located in west Texas and consist of approximately 358 miles of pipeline across the Permian and Delaware basins. During 2012, average throughput on the Company's gathering systems was 0.076 billion cubic feet per day. The Company's Permian Basin gathering systems are connected to pipelines in the area owned by Southern Union, Enterprise, West Texas Gas, CDP Midstream and Regency. Natural gas delivered into these transportation pipelines is re-delivered into the Waha hub and El Paso Gas Transmission. The Waha hub serves the Texas intrastate electric power plants and heating market, as well as the Houston Ship Channel chemical and refining markets. El Paso Gas Transmission serves western the United ! States ma! rkets.

Other Mid-Continent Regions

The Company's other Mid-Continent region assets consist of systems in the Ardmore Basin in Oklahoma, the Arkoma Basin in eastern Oklahoma and western Arkansas and the East Texas and Gulf Coast regions of Texas. The other Mid-Continent assets include approximately 648 miles of pipeline. These gathering systems are localized systems gathering specific production for re-delivery into established pipeline markets. During 2012, average throughput on these gathering systems was 0.031 billion cubic feet per day.

The Company competes with Energy Transfer Partners, Crosstex Energy, Crestwood Midstream Partners, Freedom Pipeline, Peregrine Pipeline, XTO Energy, EOG Resources, DFW Mid-Stream, Enbridge Energy Partners, DCP Midstream, Enterprise Products Partners Inc., Regency Energy Partners, Texstar Midstream Operating, West Texas Gas Inc., TGGT Holdings, Kinderhawk Field Services, CenterPoint Field Services, Williams Partners, Penn Virginia Resource Partners, Caiman Energy, MarkWest Energy Partners, Kinder Morgan, Dominion Transmission (Blue Racer), Enogex and Atlas Pipeline Partners.

Top Oil Stocks To Own For 2014: Transocean Inc.(RIG)

Transocean Ltd. provides offshore contract drilling services for oil and gas wells worldwide. It offers deepwater and harsh environment drilling, oil and gas drilling management, and drilling engineering and drilling project management services. The company also offers well and logistics services. In addition, it engages in oil and gas exploration, development, and production activities primarily in the United States offshore Louisiana and Texas, and in the United Kingdom sector of the North Sea. As of February 10, 2011, the company owned, had partial ownership interests in, and operated 138 mobile offshore drilling units, including 47 high-specification floaters, 25 midwater floaters, 9 high-specification jackups, 54 standard jackups, and 3 other rigs, as well as 1 ultra-deepwater floater and 3 high-specification jackups under construction. Transocean Ltd. was founded in 1953 and is based in Zug, Switzerland.

Advisors' Opinion:- [By Matt DiLallo]

As a contract driller this company works with large international oil companies to drill for oil and gas.�It has one of the largest fleets in the business, currently second only to Transocean (NYSE: RIG ) . Also worth noting, the company isn't as directly�affected by commodity prices as the exploration and production�companies�that contracts with it.���

Top Oil Stocks To Own For 2014: Noble Corp (NE)

Noble Corporation is an offshore drilling contractor for the oil and gas industry. The Company performs contract drilling services with its fleet of 79 mobile offshore drilling units and one floating production storage and offloading unit (FPSO) located globally. As of December 31, 2011, its fleet consisted of 14 semisubmersibles, 14 drillships, 49 jackups and two submersibles. Its fleet includes 11 units under construction, which include five ultra-deepwater drillships, and six jackup rigs. As of February 15, 2012, approximately 84% of its fleet was located outside the United States in areas, which included Mexico, Brazil, the North Sea, the Mediterranean, West Africa, the Middle East, India and the Asian Pacific. During the year ended December 31, 2011, it completed construction on the Noble Bully I, a drillship, owned through a joint venture with a subsidiary of Royal Dutch Shell plc; completed construction on the Noble Bully II, a drillship, and it completed construction of Globetrotter-class drillship. As of February 15, 2012, it had 10 rigs under contract in Mexico with Pemex Exploracion y Produccion (Pemex).

During 2011, the Company conducted offshore contract drilling operations, which accounted for over 98% of its operating revenues. It conducts its contract drilling operations in the United States Gulf of Mexico, Mexico, Brazil, the North Sea, the Mediterranean, West Africa, the Middle East, India and the Asian Pacific. During 2011, revenues from Shell and its affiliates accounted for approximately 24% of its total operating revenues. During 2011, revenues from Petroleo Brasileiro S.A. (Petrobras) accounted for approximately 18% and 19% of its total operating revenues. Revenues from Pemex accounted for approximately 15%, 20% and 23% of its total operating revenues.

Semisubmersibles

Semisubmersibles are floating platforms which, by means of a water ballasting system, can be submerged to a predetermined depth so that a substantial portion of the hull is b! elow the water surface during drilling operations. As of December 31, 2011, the semisubmersible fleet consisted of 14 units, including five Noble EVA-4000 semisubmersibles; three Friede & Goldman 9500 Enhanced Pacesetter semisubmersibles; two Pentagone 85 semisubmersibles; two Bingo 9000 design unit submersibles; one Aker H-3 Twin Hull S1289 Column semisubmersible, and one Offshore Co. SCP III Mark 2 semisubmersible.

Drillships

The Company�� drillships are self-propelled vessels. These units maintain their position over the well through the use of either a fixed mooring system or a computer controlled dynamic positioning system. Its drillships are capable of drilling in water depths from 1,000 to 12,000 feet. The maximum drilling depth of its drillships ranges from 20,000 feet to 40,000 feet. As of December 31, 2011, the drillship fleet consisted of 14 units, including four drillships under construction with Hyundai Heavy Industries Co. Ltd. (HHI); three Gusto Engineering Pelican Class drillships; two Bully-class drillships to be operated by it through a 50% joint venture with a subsidiary of Shell; one dynamically positioned Globetrotter-class drillship that left the shipyard during the fourth quarter of 2011; one Globetrotter-class drillship under construction; one moored Sonat Discoverer Class drillship capable of drilling in Arctic environments; one NAM Nedlloyd-C drillship, and one moored conversion class drillship.

Jackups

As of December 31, 2011, the Company had 49 jackups in its fleet, including six jackups under construction. The rig hull includes the drilling rig, jacking system, crew quarters, loading and unloading facilities, storage areas for bulk and liquid materials, helicopter landing deck and other related equipment. All of its jackups are independent leg and cantilevered. Its jackups are capable of drilling to a maximum depth of 30,000 feet in water depths up to 400 feet.

Submersibles

The Company has two su! bmersible! s in the fleet, which are cold-stacked. Submersibles are mobile drilling platforms, which are towed to the drill site and submerged to drilling position by flooding the lower hull until it rests on the sea floor, with the upper deck above the water surface. Its submersibles are capable of drilling to a depth of 25,000 feet in water depths up to 70 feet.

Advisors' Opinion:- [By Travis Hoium]

The second quarter wasn't a blowout for Noble (NYSE: NE ) but it was an incremental improvement without the help of new drilling rigs to boost results. It really sets a solid foundation until new rigs commanding high dayrates will begin contributing to revenue.

- [By Paul Ausick]

Two oil field services companies announced on Tuesday that they plan to spin off parts of their businesses into separately traded companies. National Oilwell Varco Inc. (NYSE: NOV) will hive off its distribution business, and Noble Corp. (NYSE: NE) plans to spin off its standard specification (shallow-water) drilling units.

- [By Rich Duprey]

For the second time in five years, oil giant Noble (NYSE: NE ) wants to pick up stakes and move. It announced today that its board of directors approved a move from its current location in Switzerland to a new home in the United Kingdom. The move would need to be approved by shareholders.�In 2008, the Houston-based driller had been incorporated in the Cayman Islands and moved to Switzerland to take advantage of preferential tax treatments there.

- [By Claudia Assis]

Noble (NE) , one of the world�� largest offshore drillers, said late Tuesday it would spin off its that may go public next year.

Top Oil Stocks To Own For 2014: Transportadora de Gas del Sur SA (TGS)

Transportadora de Gas del Sur S.A. (TGS) is engaged in the transportation of natural gas and production and commercialization of natural gas liquids (NGL). TGS�� pipeline system connects major gas fields in southern and western Argentina with gas distributors and industries in those areas and in the greater Buenos Aires area. The Company also renders midstream services, which consist of gas treatment, removal of impurities from the natural gas stream, gas compression, wellhead gas gathering and pipeline construction, operation, and maintenance services. The Company operates in three segments: natural gas transportation services through its pipeline system; NGL production and commercialization, and other services, which include midstream and telecommunication services.

During the year ended December 31, 2009, the Company�� gas transportation represented approximately 42% of total net revenues. During 2009, its NGL production and commercialization segment accounted for 50% of the total revenues of the Company. During 2009, its other services segment accounted for 8% of total revenues of the Company. Its other services segment consists of midstream and telecommunications services. Through midstream services, TGS provides integral solutions related to natural gas from wellhead up to the transportation systems. The services consists of gas gathering, compression and treatment, as well as construction, operation and maintenance of pipelines, which are generally rendered to natural gas and oil producers at wellhead. The customers��portfolio also includes distribution companies, industrial users, power plants and refineries.

During 2009, the Company provided a range of technical services to different customers. The services consisted of connections to the transportation system, engineering inspections, project management and professional technical counseling. Telecommunication services are provided through Telcosur S.A. (Telcosur), who renders services both as an independent c! arrier of carriers and to corporate clients within its area. Telcosur has a digital land radio connection system.

Advisors' Opinion:- [By Dividend]

Transportadora de Gas Del Sur S.A. (TGS) has a market capitalization of $308.26 million. The company employs 829 people, generates revenue of $466.44 million and has a net income of $43.33 million. Transportadora de Gas Del Sur�� earnings before interest, taxes, depreciation and amortization (EBITDA) amounts to $170.33 million. The EBITDA margin is 36.52 percent (the operating margin is 27.41 percent and the net profit margin 9.29 percent).

- [By Corinne Gretler]

TGS (TGS) slumped 7.4 percent to 176.90 kroner as Norway�� largest surveyor of underwater oil-and-gas fields lowered its forecast for full-year revenue to $920 million to $1 billion because of lower-than-expected demand from industry. It had projected sales of $970 million to $1.05 billion.

- [By Sofia Horta e Costa]

Telecom Italia SpA (TIT) lost 1.8 percent as Standard & Poor�� said it may downgrade the phone company�� debt to non-investment grade. TGS Nopec Geophysical Co. (TGS) tumbled the most in two years after reducing its revenue forecast. Celesio AG jumped to a three-year high on a report that McKesson Corp. may buy the German drug distributor.

Top Oil Stocks To Own For 2014: Magellan Midstream Partners L.P.(MMP)

Magellan Midstream Partners, L.P., together with its subsidiaries, engages in the transportation, storage, and distribution of refined petroleum products and crude oil in the United States. Its pipeline system transports petroleum products and liquefied petroleum gases from the Gulf Coast refining region of Texas through the Midwest to Colorado, North Dakota, Minnesota, Wisconsin, and Illinois. The company owns and operates marine terminals, which store and distribute refined petroleum products, blendstocks, crude oils, heavy oils, and feedstocks, as well as inland terminals that consist of storage tanks connected to third-party interstate pipeline systems to deliver refined petroleum products. Its ammonia pipeline system transports ammonia from production facilities in Texas and Oklahoma to terminals in the Midwest. The company also stores, blends, and distributes biofuels, such as ethanol and biodiesel. As of March 31, 2011, it operated approximately 9, 600 miles of petr oleum products pipeline system and 51 terminals; 6 marine petroleum terminals located along the United States Gulf and East Coasts; a crude oil storage in Cushing, Oklahoma; 27 petroleum products inland terminals located principally in the southeastern United States; and a 1,100-mile ammonia pipeline system and 6 associated terminals. The company also provides ancillary services, such as heating, blending, and mixing of stored petroleum products and additive injection services. Its customers comprise independent and integrated oil companies, wholesalers, retailers, railroads, airlines, and regional farm co-operatives. The company serves various markets, including retail gasoline stations, truck stops, farm co-operatives, railroad fueling depots, and military and commercial jet fuel users. Magellan GP, LLC serves as the general partner of the company. The company was founded in 2000 and is based in Tulsa, Oklahoma.

Advisors' Opinion:- [By Dividends4Life]

Magellan Midstream Partners LP (MMP) is engaged in the transportation, storage and distribution of refined petroleum products primarily through its 9,600-mile pipeline system.

Yield: 3.9% | Years of Dividend Growth: 12 - [By Arjun Sreekumar]

Additionally, new and reversed pipelines are allowing more crude oil to flow directly from oil and gas hot spots, such as the Permian Basin of West Texas, to Gulf Coast refineries. For instance, Magellan Midstream Partners' (NYSE: MMP ) started up its reversed Longhorn pipeline in April, which provided another 225,000 barrels per day of incremental capacity from West Texas to Houston-area refineries, while Sunoco Logistics Partners (NYSE: SXL ) is expected to start up its Permian Express project this month, which will provide additional capacity out of the Permian Basin of about 90,000 barrels per day.

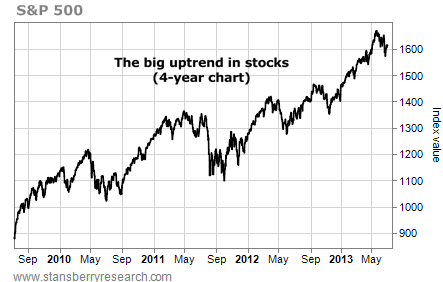

Old market hands say it's reasonable – even healthy – for a bull market to "retrace" 50% of a big gain before heading higher. If the S&P 500 retraces 50% of the gain it saw from its bottom in November to its high last month, it would decline an additional 6.5% to reach the 1,511 area. We'll keep an eye on that level... But until stocks fall that far, we'll consider the uptrend intact.

Old market hands say it's reasonable – even healthy – for a bull market to "retrace" 50% of a big gain before heading higher. If the S&P 500 retraces 50% of the gain it saw from its bottom in November to its high last month, it would decline an additional 6.5% to reach the 1,511 area. We'll keep an eye on that level... But until stocks fall that far, we'll consider the uptrend intact.